11 Years of Jan Dhan Yojana: From ₹1,000 Balances to ₹2.65 Lakh Crore Deposits – India’s Banking Revolution in Data

Introduction

On 28 August 2014, Prime Minister Narendra Modi announced the launch of the Pradhan Mantri Jan Dhan Yojana (PMJDY). The promise was simple but ambitious: every household in India should have a bank account.

At the time, many economists and bankers were skeptical. Would the poor really use bank accounts? Would they just remain “zero balance”? Was it worth the cost?

Eleven years later, the data tells a very different story. As of 20th August 2025, PMJDY has:

- 56.2 crore accounts

- ₹2.65 lakh crore deposits

- 38.7 crore RuPay debit cards

And more importantly, the average deposit per account has quadrupled, rising from ₹1,065 in 2015 to ₹4,723 in 2025. Far from being dormant, Jan Dhan accounts have become the backbone of India’s savings, welfare transfers, and digital payments ecosystem. This rise in financial inclusion mirrors other expansions in India’s formal financial base, such as the surge in PAN card holders over the last two decades.

This is the story of how Jan Dhan reshaped India’s financial landscape – year by year, rupee by rupee.

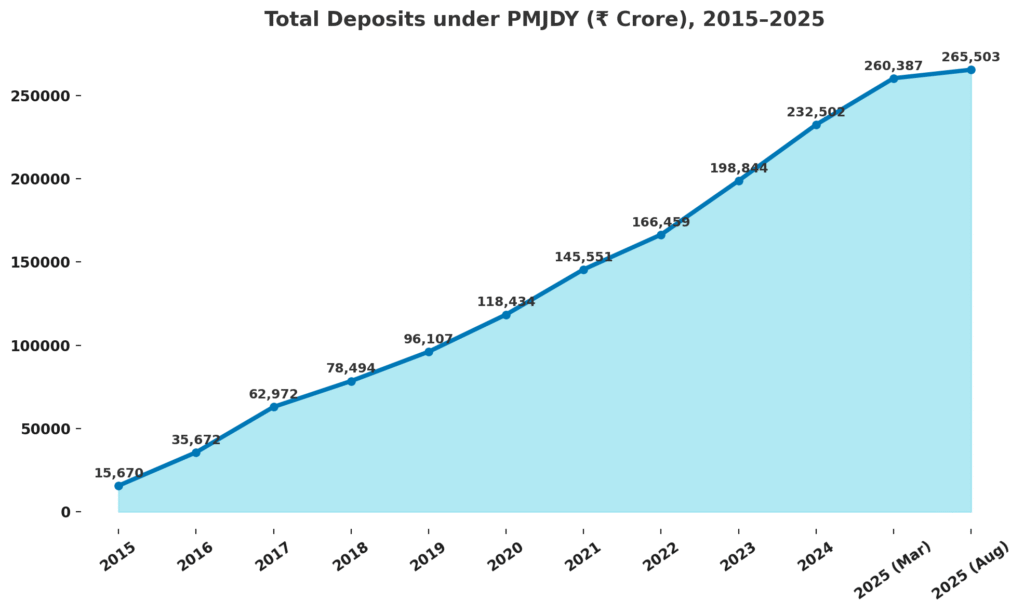

The Yearly Growth Story (2015–2025)

The scale of change becomes clear when we track PMJDY’s progress every year.

PMJDY Growth (2015–2025)

(As of March each year; latest Aug 20, 2025 data)

| Year | Accounts (Cr) | Deposits (₹ Cr) | Avg. Deposit (₹) | RuPay Cards (Cr) |

|---|---|---|---|---|

| Mar 2015 | 14.72 | 15,670 | 1,065 | 13.15 |

| Mar 2016 | 21.43 | 35,672 | 1,665 | 17.75 |

| Mar 2017 | 28.17 | 62,972 | 2,235 | 21.99 |

| Mar 2018 | 31.44 | 78,494 | 2,497 | 23.65 |

| Mar 2019 | 35.27 | 96,107 | 2,725 | 27.91 |

| Mar 2020 | 38.33 | 1,18,434 | 3,090 | 29.30 |

| Mar 2021 | 42.20 | 1,45,551 | 3,449 | 30.90 |

| Mar 2022 | 45.06 | 1,66,459 | 3,694 | 31.62 |

| Mar 2023 | 48.65 | 1,98,844 | 4,087 | 32.94 |

| Mar 2024 | 51.95 | 2,32,502 | 4,475 | 35.35 |

| Mar 2025 | 55.18 | 2,60,387 | 4,719 | 37.85 |

| 20 Aug 2025 | 56.21 | 2,65,503 | 4,723 | 38.71 |

Yearly Highlights

- 2015–16: The first full year saw explosive growth, from 14.7 to 21.4 crore accounts. Deposits more than doubled as DBT pilots began.

- 2017–18: Deposits crossed ₹78,000 crore. Average balances rose above ₹2,000, showing that accounts weren’t lying idle.

- 2019–20: With the economy digitising, RuPay cards neared 30 crore. By March 2020, average balances crossed ₹3,000.

- 2020–21 (COVID year): Relief payments flowed directly into Jan Dhan accounts. Deposits surged to ₹1.45 lakh crore, proving PMJDY’s resilience in crisis.

- 2022–23: Deposits touched nearly ₹2 lakh crore. Women and rural account shares remained steady at ~56% and ~67%.

- 2024–25: Growth slowed, but deposits kept climbing. By August 2025, India held ₹2.65 lakh crore in Jan Dhan savings.

Insight: Jan Dhan matured from an account-opening drive into a savings and transfer platform, cementing its role in India’s financial system.

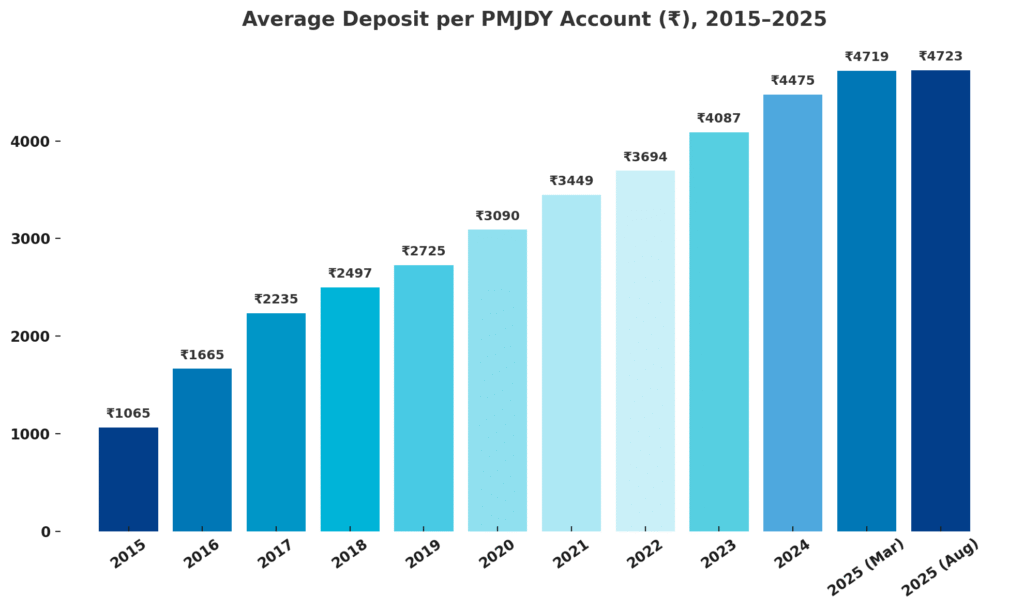

The Balance Shift — From Symbolic to Substantial

In March 2015, the average Jan Dhan account held ₹1,065 – less than a day’s wage in many cities. Critics joked these were “empty accounts.”

By August 2025, the average balance is ₹4,723. That’s a 4.4x increase in just over a decade.

This rise came from three forces:

- Direct Benefit Transfers (DBT): ₹6.9 lakh crore was credited in FY 2024–25 alone.

- Savings Habit Formation: With interest on deposits and easy access, families began using accounts as real savings tools.

- Rural Inclusion: Seasonal workers, farmers, and women SHGs found banking safety nets for their earnings.

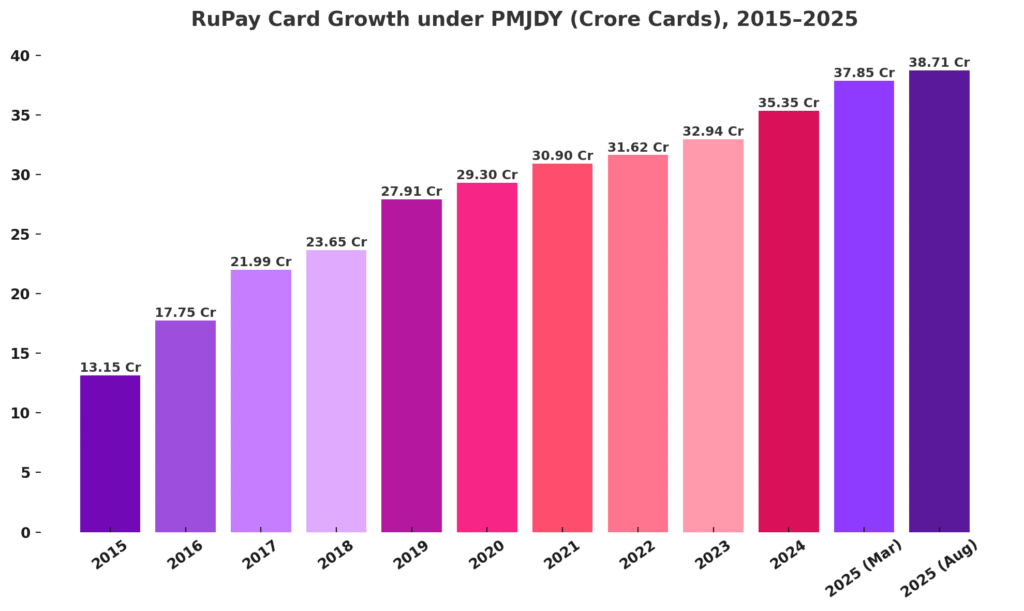

The RuPay Revolution

When Jan Dhan began, the free RuPay debit card was often seen as just an extra feature. But it has become one of PMJDY’s most powerful tools:

- Cards issued rose from 13.2 crore in 2015 to 38.7 crore in 2025.

- These cards provide ₹2 lakh accident insurance, critical for low-income households.

- They drive digital adoption: RuPay transactions at PoS & e-commerce sites rose from 67 crore (FY 2017–18) to nearly 94 crore (FY 2024–25).

For many, the RuPay card was the first step into India’s digital economy.

| Year | Cards Issued (Cr) |

|---|---|

| 2015 | 13.15 |

| 2020 | 29.30 |

| 2025 | 38.71 |

Rural India & Women Lead the Way

As ofAs of 20 August 2025:

- 67% of Jan Dhan accounts are in rural and semi-urban areas.

- 56% are owned by women. A milestone that mirrors broader trends in India’s women workforce participation

This is unprecedented. For millions of rural women, a Jan Dhan account was their first financial asset in their own name.

- Under PM Suraksha Bima and PM Jeevan Jyoti Bima, insurance coverage became accessible.

- Under Atal Pension Yojana, unorganised workers began securing retirement.

- Mudra loans flowed from Jan Dhan-linked accounts, helping women entrepreneurs.

This wasn’t just banking – it was financial empowerment.

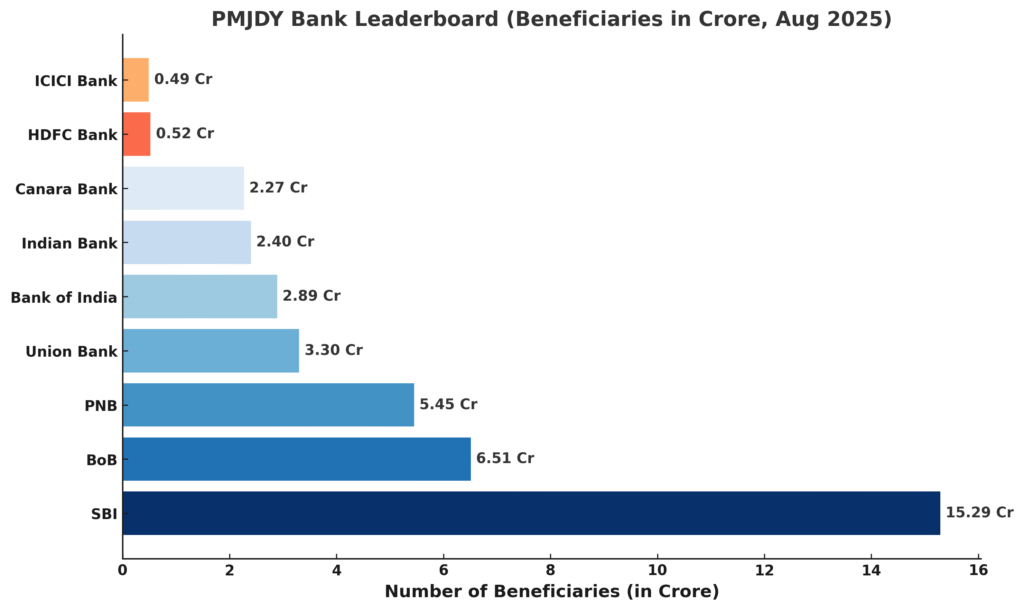

Which Banks Lead Jan Dhan? (as of Aug 13, 2025)

The bank-wise leaderboard reveals how different institutions contributed.

PMJDY Accounts by Bank Type (as of 13 Aug 2025)

| Bank Type | Total Beneficiaries (Cr) | Deposits (₹ Cr) | RuPay Cards (Cr) | Share of Total Accounts |

|---|---|---|---|---|

| Public Sector Banks | 43.56 | 20,8792 | 33.34 | 77% |

| Regional Rural Banks | 10.57 | 51,167 | 3.84 | 19% |

| Private Sector Banks | 1.84 | 7,796 | 1.49 | 3% |

| Cooperative Banks | 0.19 | negligible | 0 | <1% |

| Total | 56.16 | 2,67,756 | 38.67 | 100% |

Key Takeaway: PSU banks dominate PMJDY, handling 4 out of 5 accounts.

Top Public Banks (as of 13 Aug 2025)

| Bank | Accounts (Cr) | Deposits (₹ Cr) | RuPay Cards (Cr) |

|---|---|---|---|

| SBI | 15.29 | 67,486 | 13.37 |

| PNB | 5.45 | 24,999 | 3.99 |

| BoB | 6.51 | 35,810 | 5.97 |

| Canara Bank | 2.27 | 15,469 | 1.44 |

| Indian Bank | 2.40 | 12,113 | 1.38 |

Insight: SBI alone manages more accounts than the populations of Japan + Germany combined.

Top Private Banks (as of 13 Aug 2025)

| Bank | Accounts (Cr) | Deposits (₹ Cr) | RuPay Cards (Cr) |

|---|---|---|---|

| HDFC Bank | 0.52 | 2,960 | 0.52 |

| ICICI Bank | 0.49 | 939 | 0.47 |

| IDBI Bank | 0.22 | 753 | 0.09 |

| J&K Bank | 0.12 | 1,203 | 0.12 |

| Axis Bank | 0.14 | 937 | 0.09 |

Insight: Even the top private banks’ Jan Dhan portfolios are tiny compared to PSU giants. HDFC + ICICI combined = less than half of BoB’s Jan Dhan accounts.

The JAM Trinity in Action

The Jan Dhan–Aadhaar–Mobile (JAM) trinity turned PMJDY into the backbone of India’s subsidy delivery. By linking accounts with Aadhaar and mobile numbers:

- Subsidies reached beneficiaries directly, without leakages.

- ₹6.9 lakh crore was transferred in FY 2024–25 alone.

- DBT coverage expanded to LPG, food, fertiliser, pensions, and scholarships.

This makes Jan Dhan not just about inclusion, but about efficiency in governance. Also JAM turned Jan Dhan into the artery of India’s welfare state.

India vs the World

No other country has achieved banking access for half a billion people in one decade.

India opened 56 crore accounts in 11 years – more than the combined population of USA + EU.

The World Bank calls PMJDY “a financial inclusion miracle.”

Conclusion

From ₹1,000 balances to ₹2.65 lakh crore deposits, from 13 crore RuPay cards to nearly 39 crore, and from zero-balance accounts to 4.7x growth in deposits per person, Jan Dhan Yojana is no longer just a welfare scheme – it’s the foundation of India’s financial ecosystem.

It is now the platform that supports:

- Savings and credit access for low-income households.

- Digital transactions and UPI adoption.

- DBT transfers worth lakhs of crores.

- Women’s empowerment and rural inclusion.

Takeaway: What began in 2014 as “everyone should have a bank account” has become, in 2025, the world’s largest and most impactful banking revolution.

Source & Methodology

The data used in this report comes from official government sources:

- Press Information Bureau (PIB): Ministry of Finance press release, August 28, 2025, which provides the latest official update on the progress of Pradhan Mantri Jan Dhan Yojana (PMJDY).

- PMJDY Official Portal (Government of India): Historical bank-wise data has been sourced from the PMJDY Archive section, while the most recent numbers on accounts, deposits, and RuPay card issuance are from the live PMJDY dashboard.

FAQs on Pradhan Mantri Jan Dhan Yojana

Q1. What is Pradhan Mantri Jan Dhan Yojana (PMJDY)?

A: PMJDY is India’s flagship financial inclusion scheme launched in 2014 to provide every household access to a basic bank account.

Q2. How many Jan Dhan accounts are there in 2025?

A: As of 20 August 2025, there are 56.2 crore Jan Dhan accounts with ₹2.65 lakh crore in deposits.

Q3. How many RuPay cards have been issued under Jan Dhan?

A: 38.7 crore RuPay debit cards have been issued to PMJDY account holders as of August 2025.

Q4. What percentage of Jan Dhan accounts belong to women?

A: Around 56% of Jan Dhan accounts are owned by women, empowering financial inclusion in rural and urban India.

Interesting Reads on Indiagraphs

- PAN Card Statistics in India: Growth of Formal Identity – How India expanded its taxpayer and identity base alongside financial inclusion.

- Gold vs Sensex Returns in India – A 25-year journey comparing India’s favorite safe haven with its stock market.

- Indian Rupee vs US Dollar: Historical Performance – The story of how the rupee has fared against the world’s strongest currency.

- India’s Gold Import Data – A decade-long story of India’s gold demand, trade balances, and policy shifts.